August 25, 2025

SaaS valuation insights report highlights

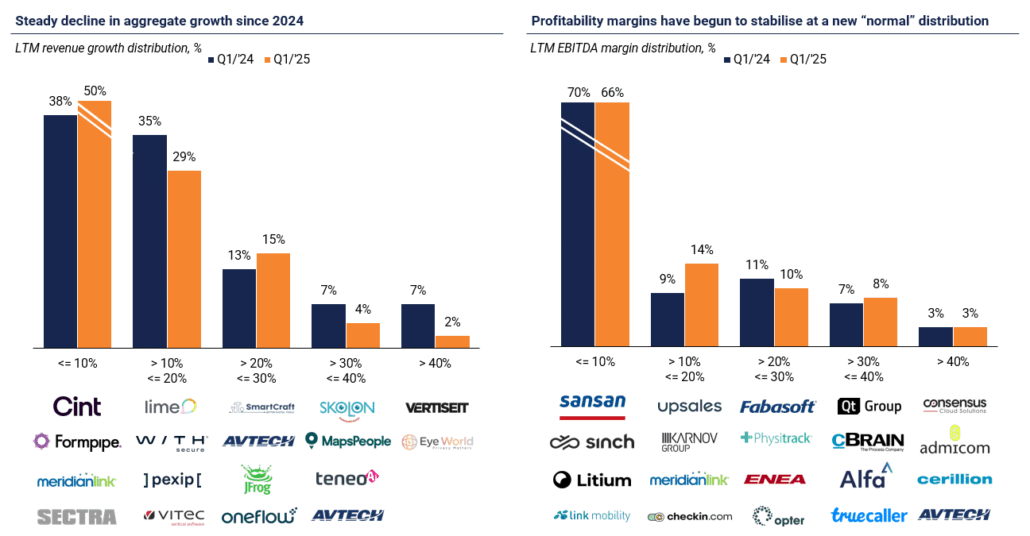

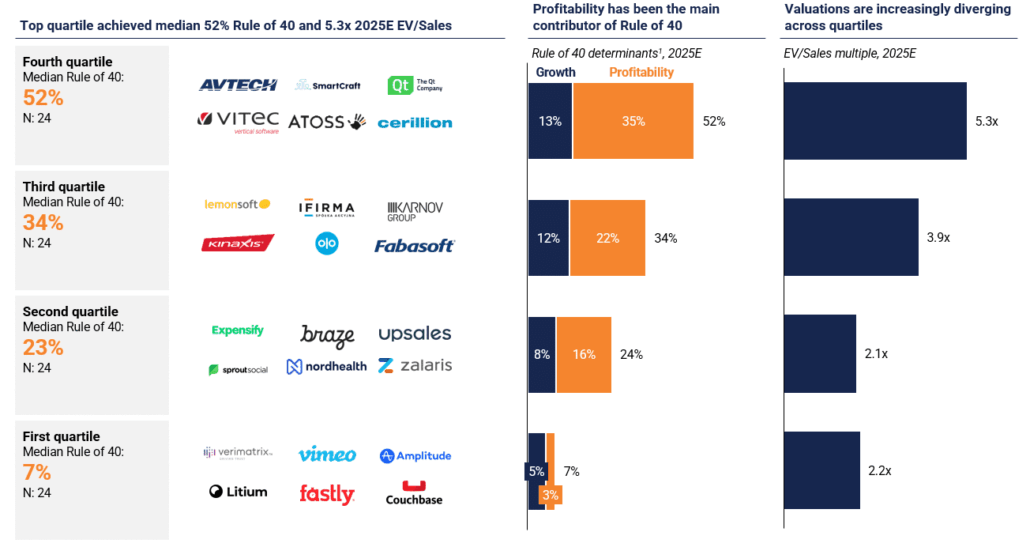

Stable multiples masking structural shifts: Since our inaugural SaaS Valuation Insights Report was published in early 2023, aggregate Nordic public SaaS valuations have remained broadly flat. Median EV/Sales multiples show little movement, but this stability masks a clear transformation happening beyond the surface: many Nordic SaaS companies are pivoting towards efficiency and improved margins, evolving into more profitable, albeit slower-growing businesses. The Rule of 40 has gradually rebalanced, with profitability increasingly outweighing the growth component.

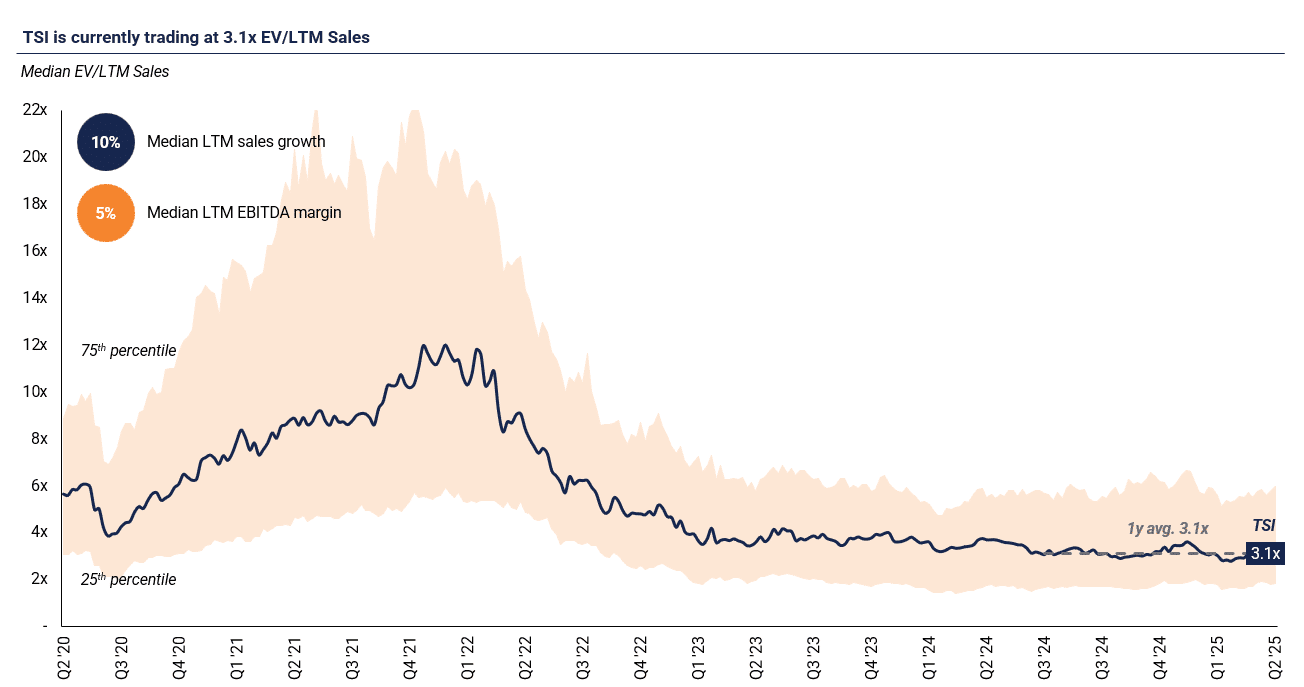

Growth remains constrained across SaaS companies: Since Q1/’23, the median EV/LTM Sales multiple has remained relatively steady at around 3.0x. Slower growth has been driven by tighter customer budgets and elongated sales cycles, while companies have responded by streamlining operations and cutting costs. This has translated into stronger margins, helping to keep the Rule of 40 metric stable at an aggregate level. That said, as this report highlights, market-wide benchmarks only provide a directional view of sentiment and performance. They should not be relied upon directly for valuation purposes.

Valuation floor at ~1.5-2x EV/Sales: Underperforming companies tend to trade just above the regression trend line, suggesting a de facto valuation floor of roughly 1.5-2x EV/Sales, even when fundamentals are very weak. A similar dynamic is evident in private market transactions, where deals often clear at or above this same level—likely reflecting the pain threshold for SaaS company owners. Notably, a large group of micro-cap and small-cap European SaaS firms currently trade near 2x EV/Sales, despite showing negative to low single-digit growth and failing to streamline operations sufficiently to reach double-digit profit margins.

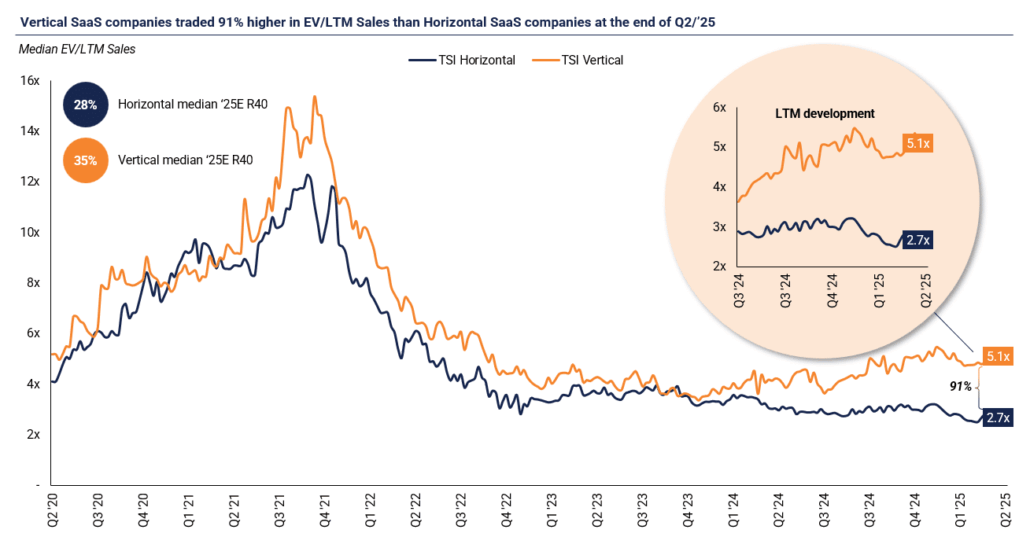

Vertical SaaS widening valuation premium: Vertical SaaS continues to trade at a clear premium to Horizontal SaaS, with the gap expanding to 91% in Q2/’25 from 77% in Q1/’25. The Rule of 40 remained steady at 35% for vertical players, while it slipped to 28% for horizontal peers (down from 30% the prior quarter), further driving the divergence. By sustaining stronger balance between growth and profitability, vertical SaaS companies have preserved investor confidence and attracted higher multiples, reinforcing the broader “flight to quality” trend also visible in private markets.

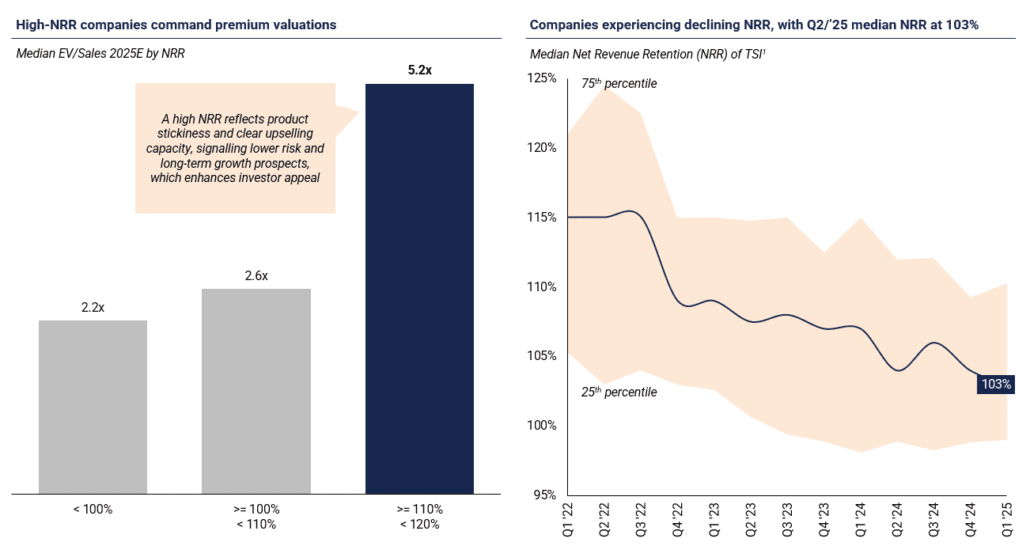

High NRR driving valuation premiums: Companies with Net Revenue Retention (NRR) above 110% command valuations roughly twice those of peers below that threshold. Elevated NRR demonstrates strong product stickiness and upselling capacity, signaling lower risk and stronger long-term growth prospects. Firms with NRR >110% trade at 5.2x EV/Sales, 68% above TSI’s median of 3.1x and nearly double the multiples of companies in the average or below-average NRR range. However, most TSI constituents are seeing NRR deterioration, with the median now at 103%.

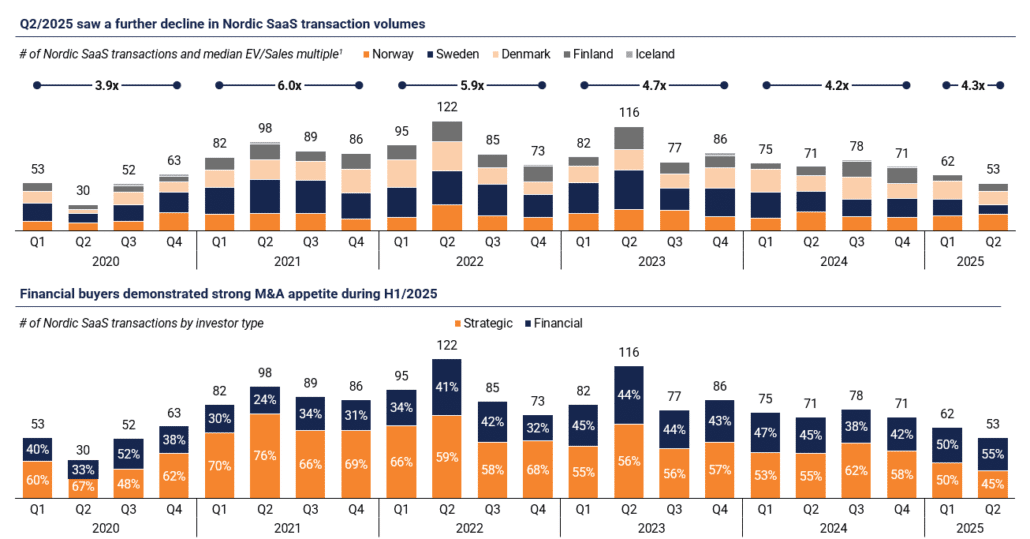

Transaction volumes continue to slide in Q2/’25: Only 53 SaaS transactions closed in the Nordics during Q2/’25, bringing the H1 total to 115 deals at a median EV/Sales multiple of 4.3x. Activity in the first half of 2025 was weaker than anticipated, marking the lowest H1 transaction count since 2020. While many analysts had initially forecasted a substantial rebound in M&A volumes and values for FY2025, expectations were significantly revised downward following the April “liberation day” tariffs and subsequent market turbulence, shifting the year onto a markedly softer trajectory. Within the large-cap segment, several widely anticipated tech and software IPOs were deferred to 2026 or postponed until further notice.

Download our SaaS valuation insights report

In our quarterly SaaS valuation insights report, we strive to provide an overview of the latest developments and trends related to valuations accompanied with our proprietary insights and learnings from live projects and observations from engaging with both clients, strategic buyers, and investors in our cross-border advisory practice.

The full SaaS valuation insights report can be downloaded by clicking the link below, and the report will also be published on our website on a quarterly basis.

Tero Nummenpää, Partner

Ruben Moring, Partner

Juuso Marttinen, Partner