26.10.2023

Our quarterly SaaS Valuation Update is centred around the Translink SaaS Index (“TSI”), providing an extensive examination of index constituents, SaaS M&A trends, and the broader European SaaS market. This update aims to present our key insights, observations, and analytical perspectives on the mid-market SaaS valuation landscape.

Distinguishing itself from other comparable indices, TSI primarily comprises small to mid-sized public SaaS companies in the Nordic and European regions. It includes 130+ companies, with 35% headquartered in the Nordics, 25% in other parts of Europe, 30% in the United States, and roughly 10% in other global markets. Importantly, our index intentionally excludes large-cap SaaS companies.

We firmly believe that our proprietary index serves as a valuable benchmark for assessing the valuations of small and mid-sized SaaS firms, which are typically the focus of transactions within our core European markets.

SaaS Valuation Update report excerpts

From peak to trough: SaaS valuations went from bizarre levels in 2020-2022 to a five-year low level in a manner of months. It may appear that current SaaS valuations are now abnormally low. The reality is that, when we factor out the impact of the Covid-19 frenzy, we find ourselves much closer to the historical long-term average.

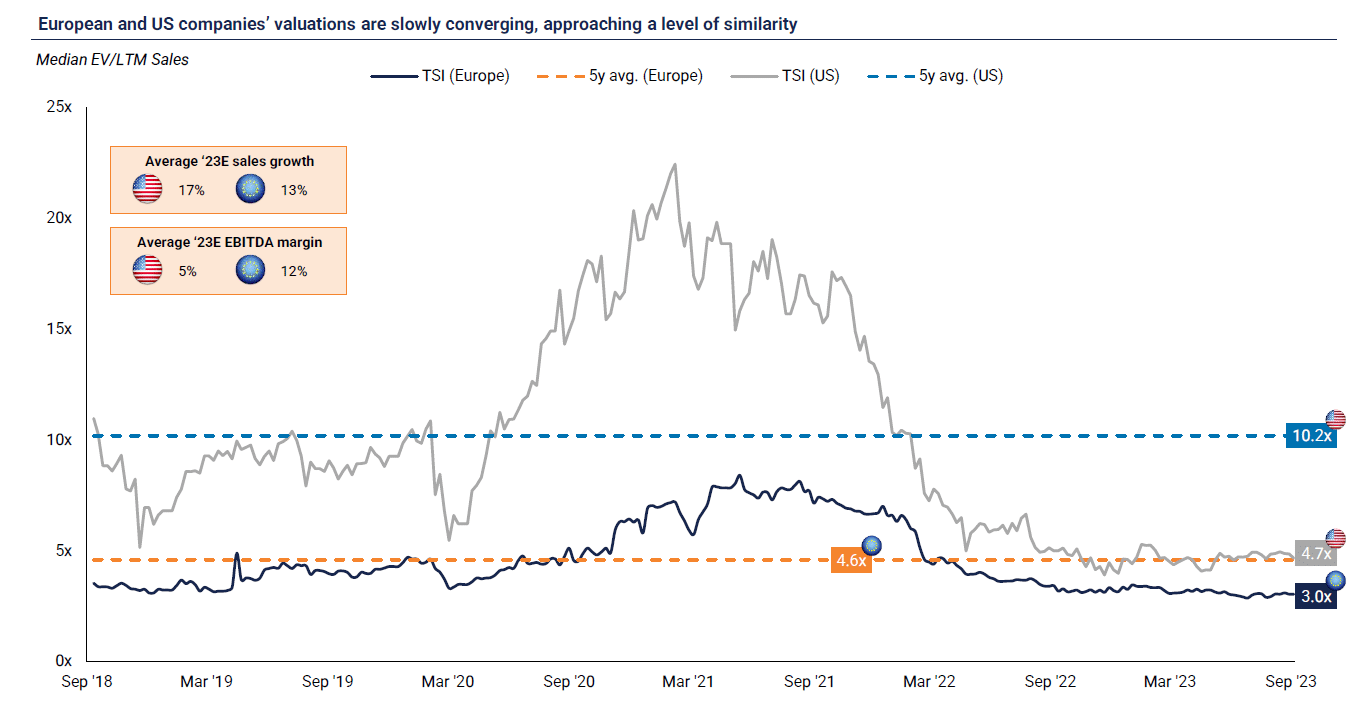

Converging valuations: European and U.S. SaaS valuations are approaching convergence due to the rising cost of capital, coupled with investor priorities shifting towards recession-resistant businesses and immediate profitability.

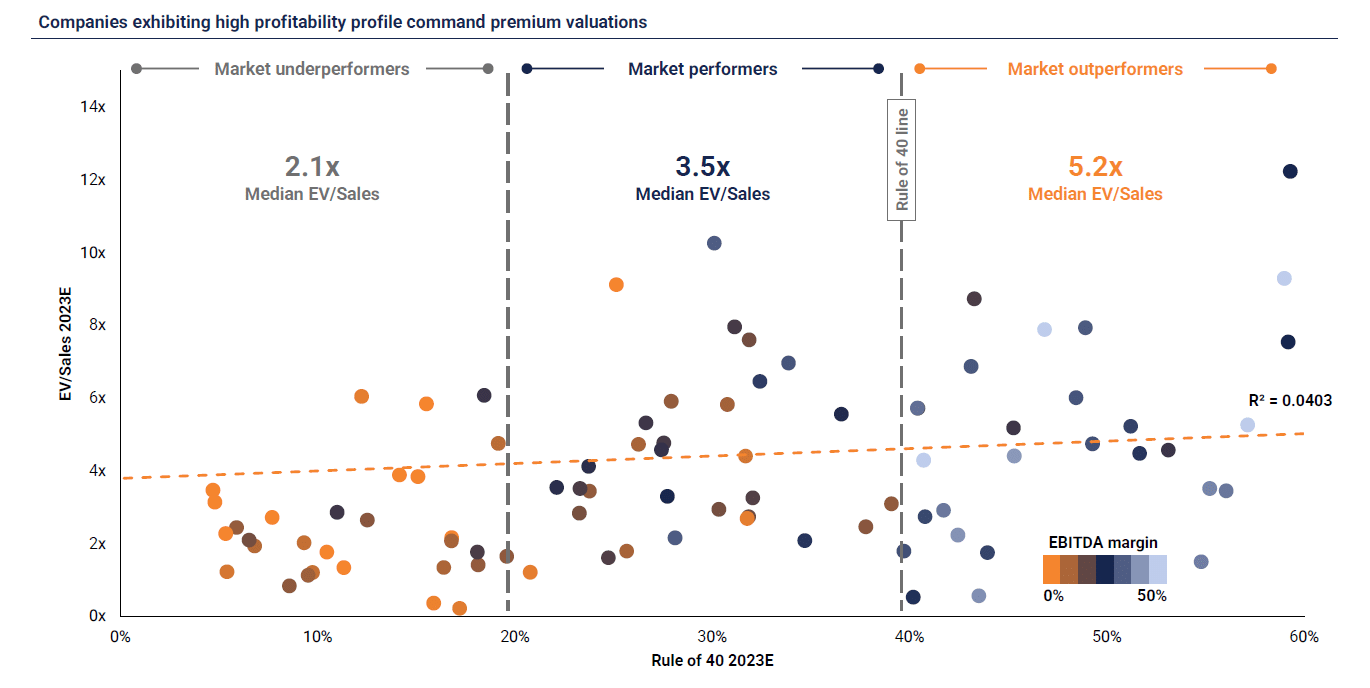

Shifting paradigm: Valuations for SaaS companies are now more closely tied to capital efficiency and profitability rather than sheer growth. Market outperformers continue to command premium valuations and trade at over 5x their projected 2023 sales.

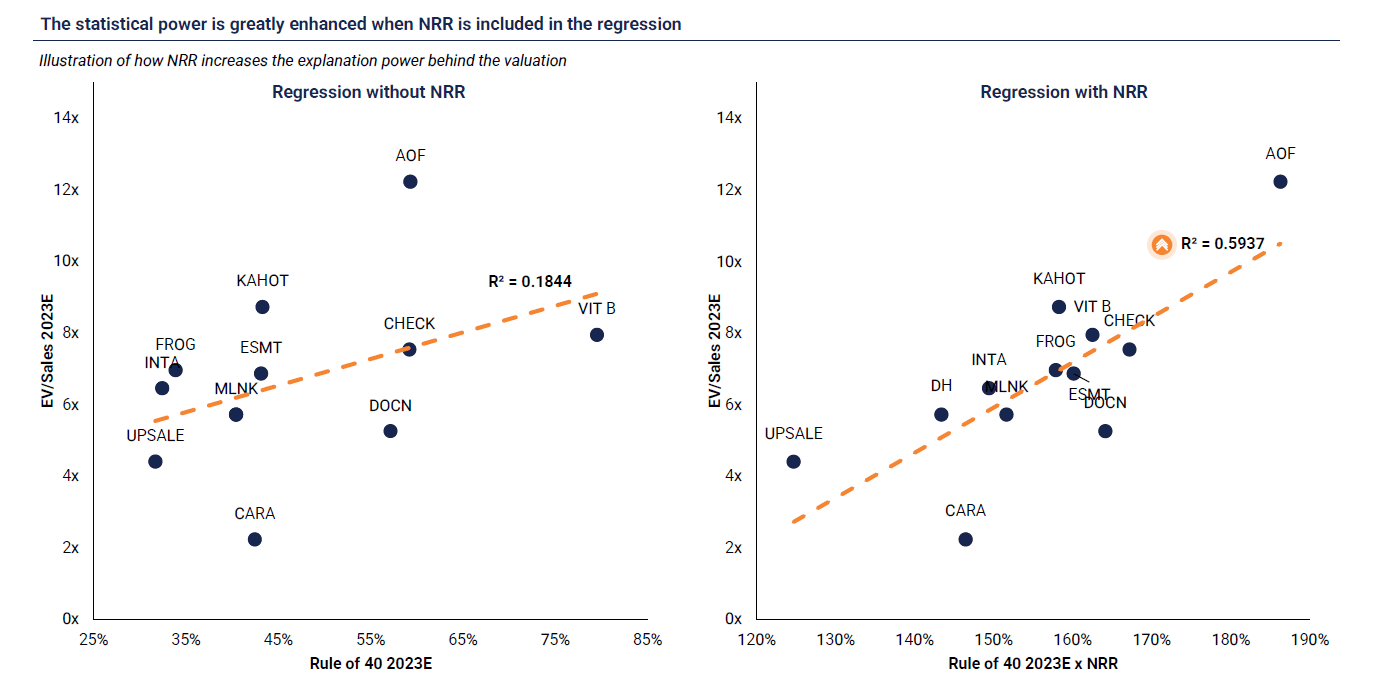

Introducing the new Rule of 40: Incorporating Net Revenue Retention into the EV/Sales and Rule of 40 metric substantially enhances the explanatory capacity for valuation.

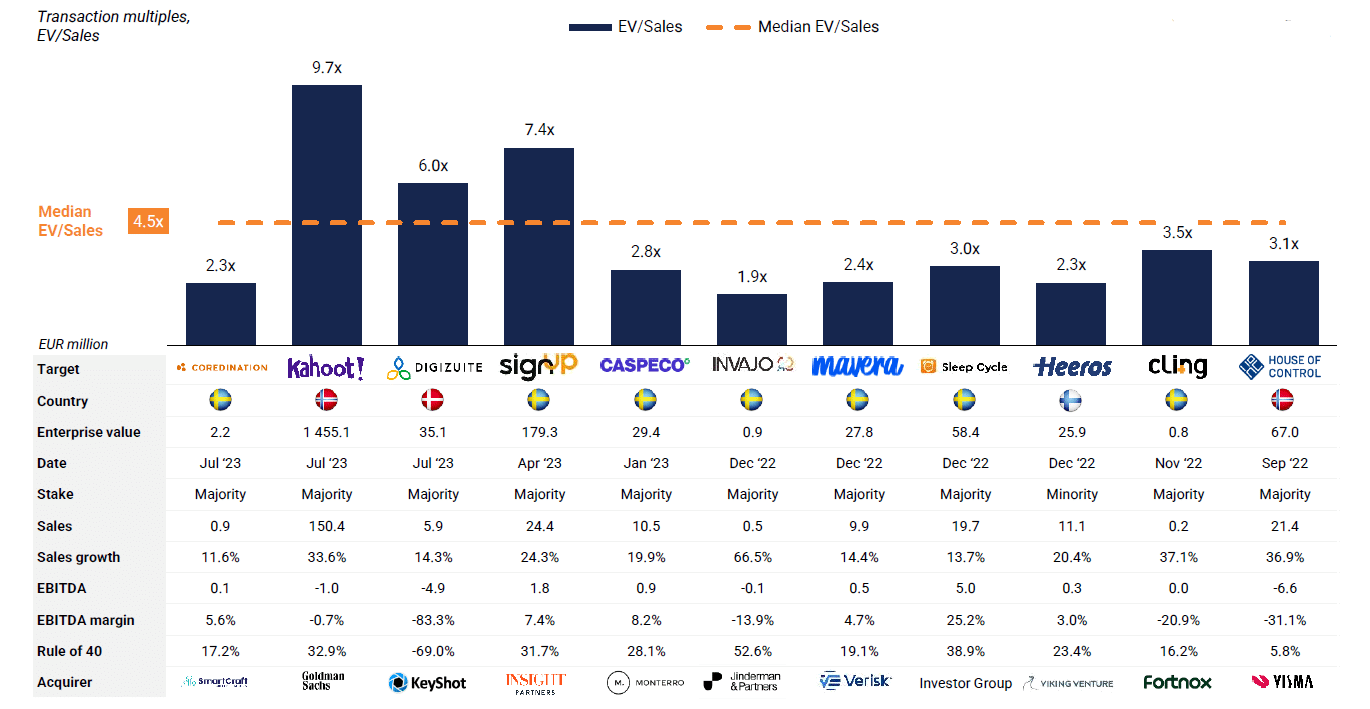

Nordic SaaS M&A continues to be robust: Despite a more demanding landscape, M&A activities persist. Nordic SaaS transactions have shown a median EV/Sales multiple of approximately 4.5x from 2020 to Q3/2023, with a median Rule of 40 metric at roughly 27%. The principle of scarcity economics remains relevant, and the pursuit of top-tier opportunities can result in outsized premiums.

We have witnessed quite a rollercoaster in SaaS valuations over the past few years

The pandemic accelerated the adoption of SaaS solutions globally, leading to remarkable revenue growth, while a low-interest rate environment created favourable conditions for fundraising and IPOs among growth-oriented companies. This, in turn, pushed valuations to unprecedented heights. However, the environment changed rapidly, with interest rates rising to levels not seen in decades, impacting the value of assets across various industries, including SaaS.

Investor perspectives also evolved, with a greater emphasis on the profitability and cash flow profiles of the businesses they invest in. In times of cheap capital, cash flows projected several years into the future held significant value, and investors were willing to wait for profitability. As the cost of capital increased, investors became more short-term-focused, resulting in multiple compression in the market. Notably, SaaS valuations experienced a more pronounced decline compared to the broader market during the 2022-H1/2023 period.

Following outsized growth rates and exceptional SaaS metrics in 2020 and 2021, numerous companies encountered challenges associated with prolonged sales cycles and deferred investment decisions. This occurred concurrently with a period marked by the most substantial interest rate increases, exerting dual pressure on SaaS companies and their valuations.

Key observations of Q3/2023

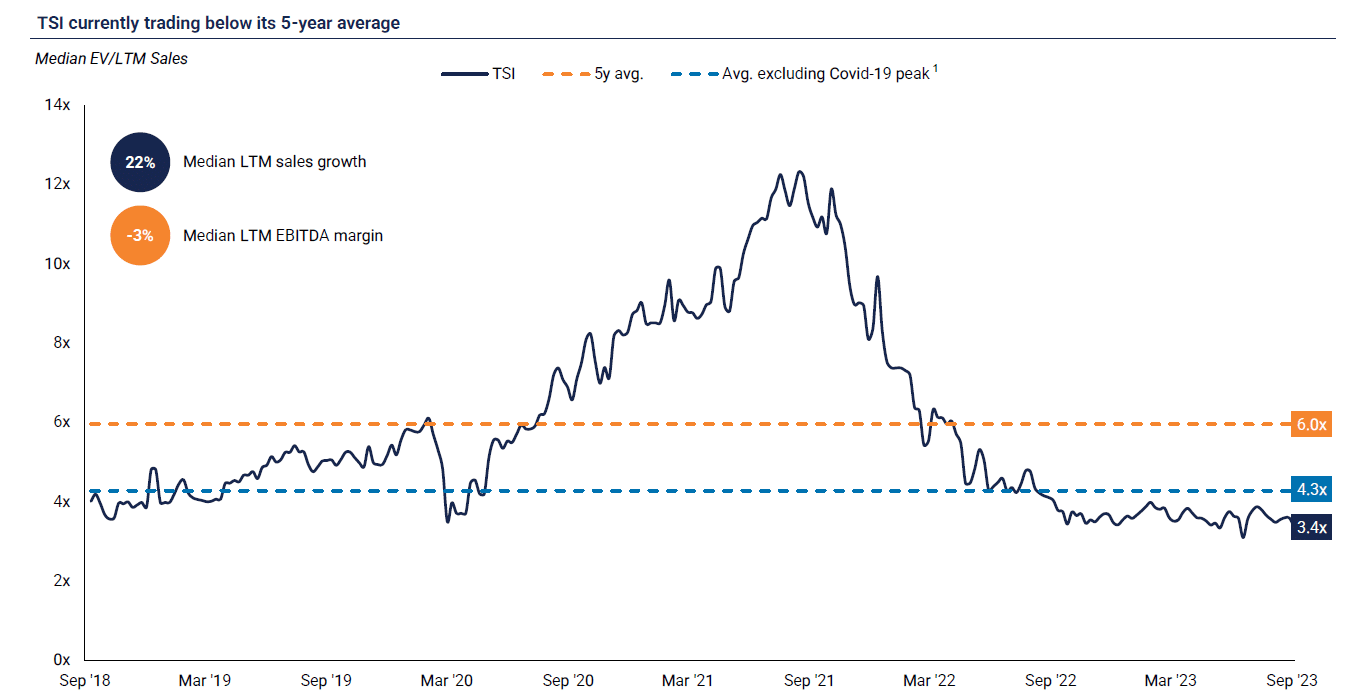

We observed a continued downward trend in SaaS valuation multiples in Q3/23. The EV/LTM Sales multiple for TSI settled at 3.4x, well below the 5-year average of 6.0x. At first glance, it looks like we are in terrible market conditions: multiples are well below their five-year averages? Yes, perhaps they are – but if we take the Covid-19 frenzy out of the average, we can see a different reality.

Excluding the Covid-19 period (Q2’20-Q2’22) from the Index, the average remains at 4.3x, about 1x above the Q2’23 EV/LTM Sales median. Nevertheless, we firmly believe that the market’s reaction has been overblown and anticipate that SaaS valuation multiples will normalise around the long-term (covid-adjusted) average as we head towards and into 2024.

While we do not foresee substantial upward pressure on valuations in the immediate future, the market is expected to adapt to the current landscape, leading to increased M&A activity in both the public and private markets. It is worth noting that companies demonstrating exceptional profitability and growth will continue to command premium valuations.

Download our SaaS Valuation Update report

In our quarterly SaaS Valuation Update, we strive to provide an overview of the latest developments and trends related to valuations accompanied with our proprietary insights and learnings from live projects and observations from engaging with both clients, strategic players, and investors in our cross-border advisory practice.

The full SaaS Valuation Update report can be downloaded below. The Valuation Update will be published on our website on a quarterly basis. Make sure to subscribe to our newsletter to get the report directly to your inbox.

Tero Nummenpää, Partner

Ruben Moring, Partner

Juuso Marttinen, Partner