6.11.2025

Nordic SaaS valuation insights report highlights

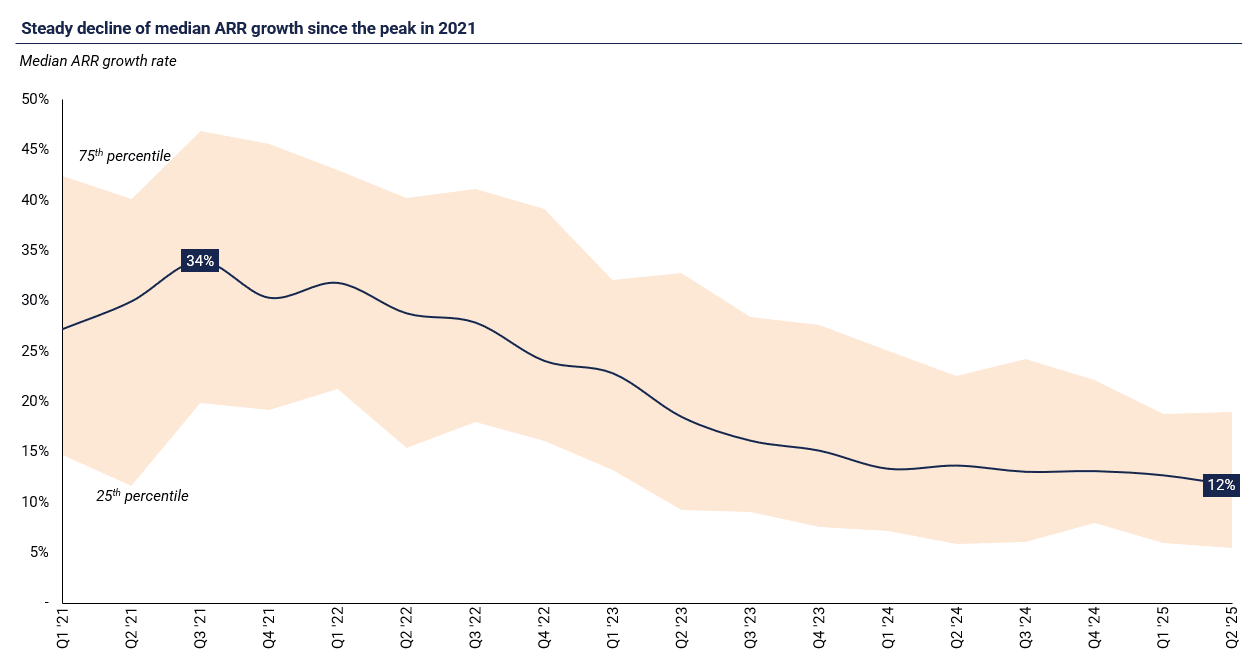

Overall ARR growth continues to decline: A clear and steady slowdown is evident from mid-2021, when the median company was growing at a robust 34%, to the end of H1/’25, when median ARR growth had dropped to 12%. Most SaaS companies are struggling to sustain strong growth momentum. A similar trend can be seen in the Rule of 40 metric. However, thanks to improving efficiency and widening profit margins, the median Rule of 40 has been on an upward trajectory since late 2023, reaching 16% by the end of H1/’25, up from 11% in Q4/’24.

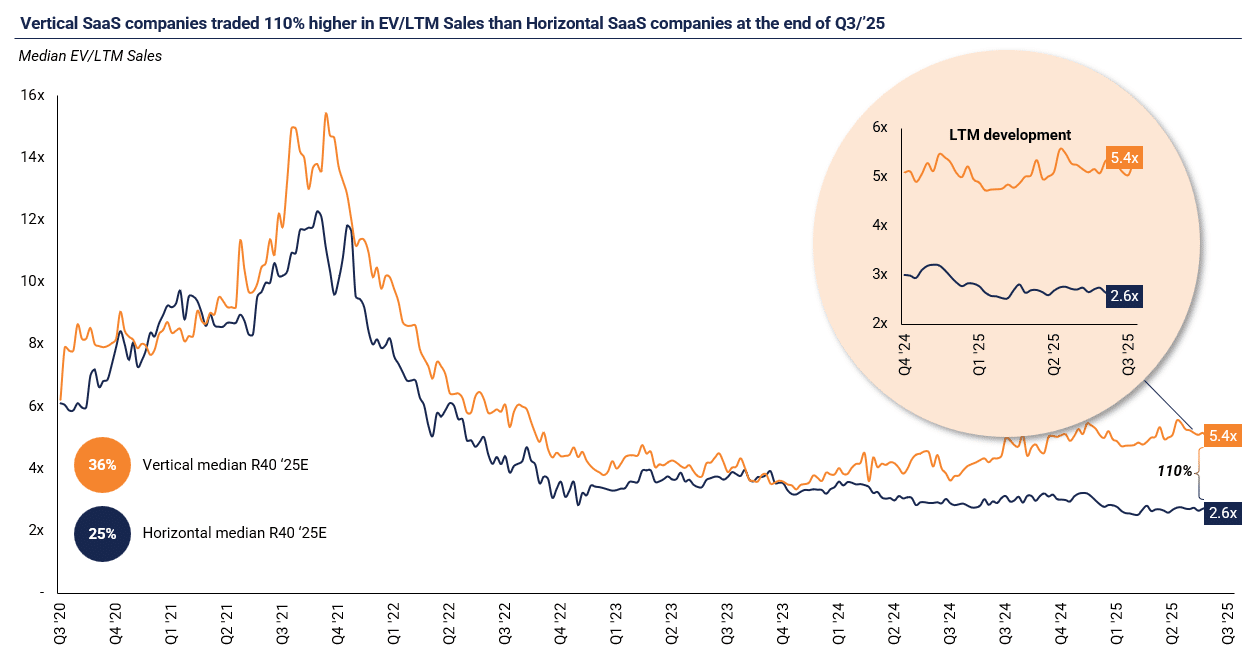

Vertical SaaS continues to outperform horizontal peers: The valuation gap between the two categories has widened further, with vertical SaaS companies now trading at a 110% premium to horizontal peers — up from 77% in Q1/’25. This growing divergence is making the categories increasingly difficult to compare directly. Therefore, our Q4/’25 report will provide separate analyses of performance and valuation metrics for each segment.

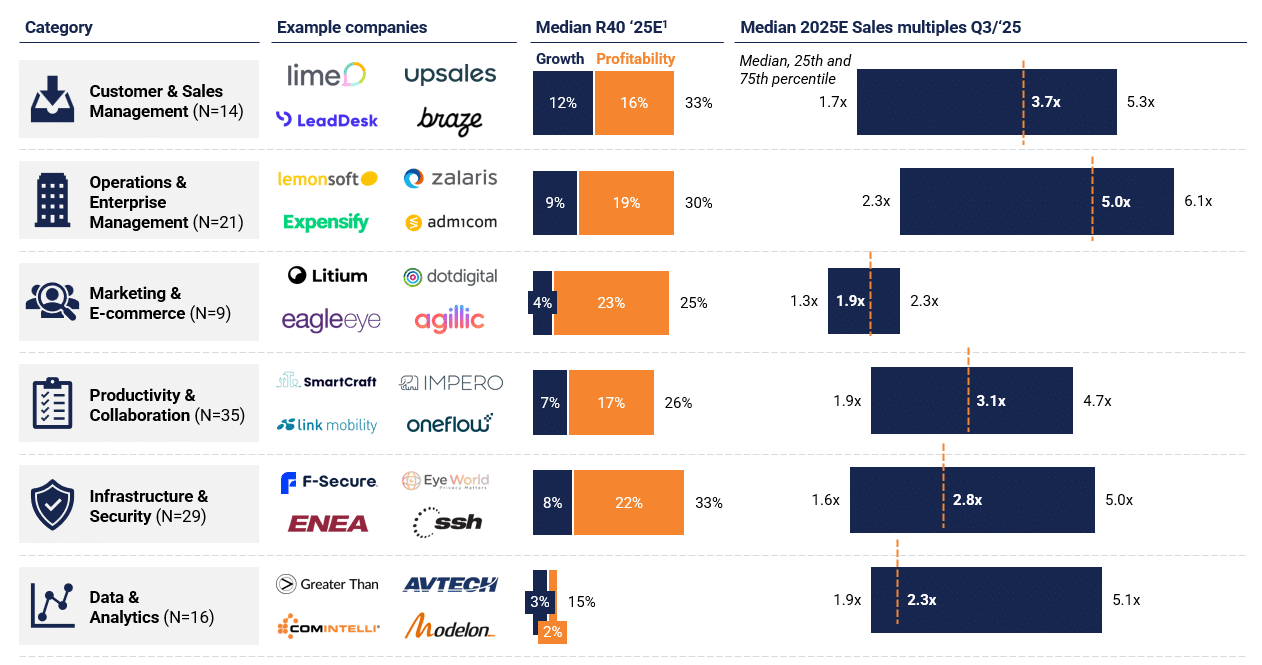

Business-critical software multiples remain resilient: Operations and enterprise management SaaS vendors continue to command a strong “stickiness premium”, even without outperforming peers on the Rule of 40 metric. Vertical core software providers have maintained solid valuation levels despite the broader market’s muted sentiment.

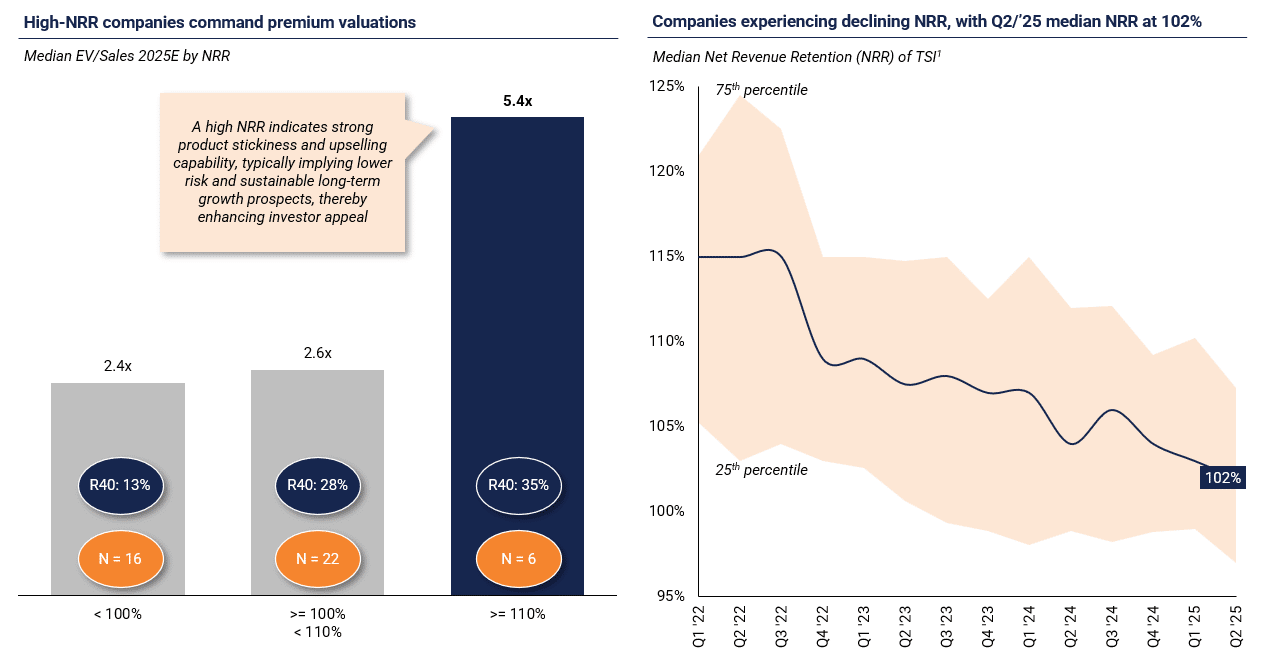

High-NRR companies trade at double the valuation of low-NRR peers: Consistent with previous reports, companies with NRR above 110% continue to command significantly higher valuations than those with lower NRR, reflecting the strong foundation high retention provides for sustainable long-term growth. These high-NRR companies also tend to outperform on the Rule of 40, reinforcing the view that strong NRR is a critical driver of durable, long-term performance.

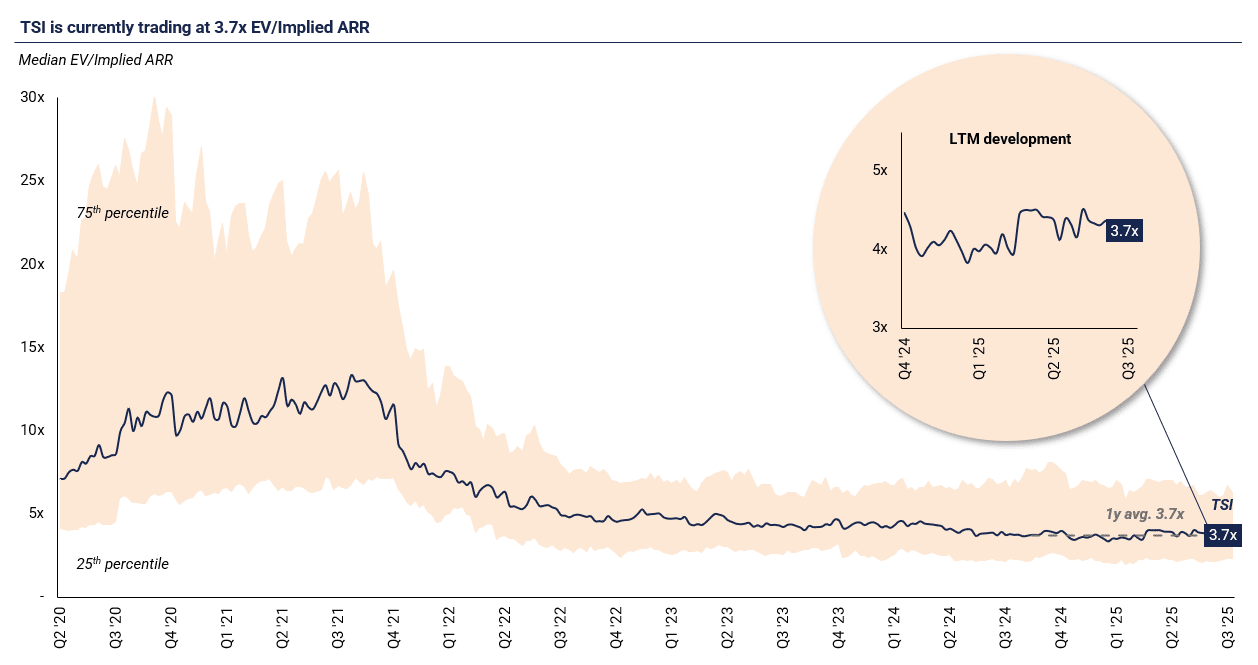

Introducing the implied EV/ARR multiple: The EV/ARR multiple, which uses annual implied recurring revenue instead of total sales as the denominator, currently stands at 3.7x, in line with the one-year average. This represents a 15% premium to the median EV/LTM Sales multiple for the same group (3.2x), partly reflecting the effect of one-off sales that inflate total sales relative to recurring revenue.

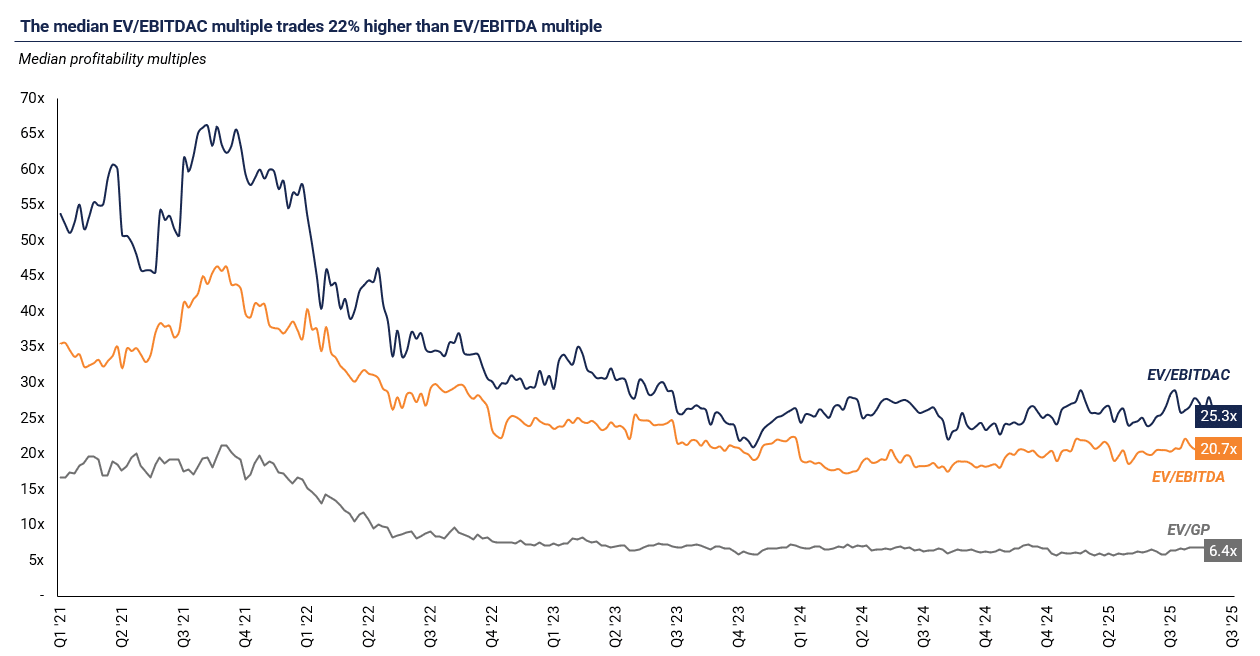

Expanding analysis of profitability multiples: With profitability now being the key driver of the Rule of 40 metric for most index constituents, we have expanded our analysis to provide a deeper review of historical performance — focusing on Gross Profit (GP), EBITDA, and EBITDAC (or Cash EBITDA, defined as EBITDA before capitalizations). Profitability multiples have remained relatively stable since late 2022, mirroring the trend seen in topline valuation metrics. The current EV/EBITDAC multiple for TSI constituents stands at 25.3x, compared to 20.7x for EV/EBITDA. This premium suggests that reported EBITDA figures are approximately 20% higher than EBITDAC, highlighting the impact of capitalized costs. Meanwhile, the EV/GP multiple remains steady at 6.4x, showing little change since mid-2022.

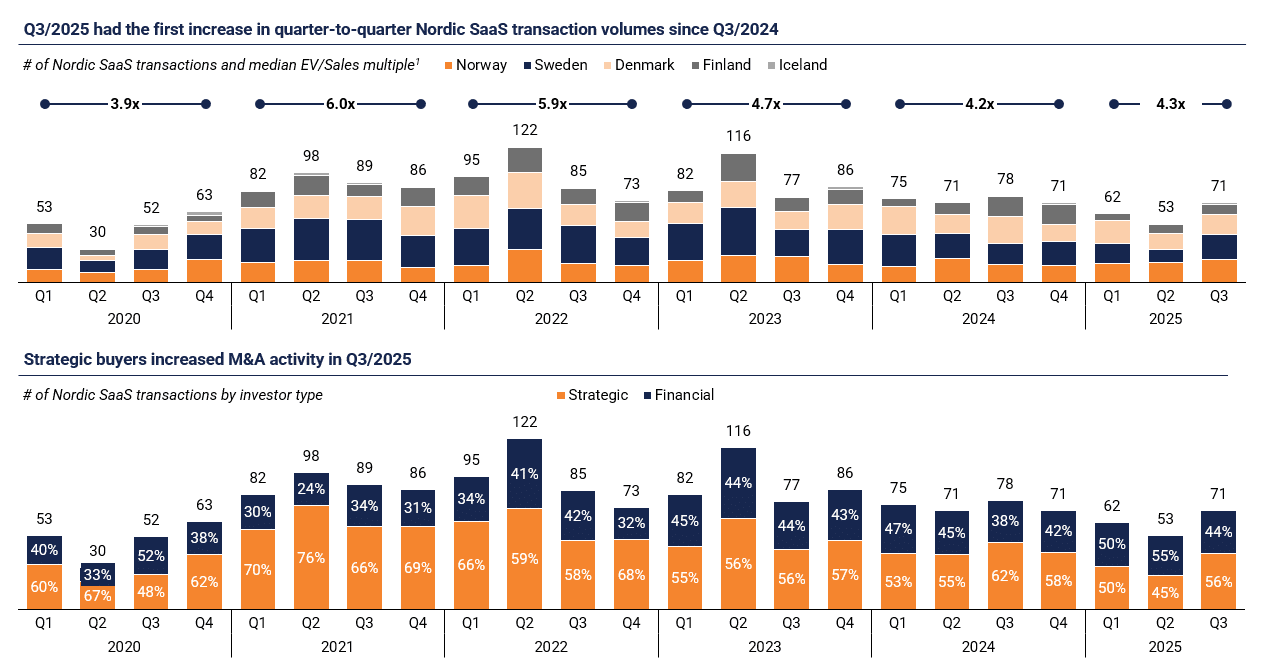

Nordic SaaS M&A activity rebounded in Q3/2025: Following a subdued Q2/’25, the Nordic SaaS M&A market saw its busiest quarter of the year, with 71 transactions completed during Q3/’25. The median EV/Sales multiple for transactions stood at 4.3x year-to-date, consistent with the previous year’s level. Notably, Sweden’s Sana Labs made headlines with one of the first major M&A deals involving a Nordic AI-native software company, valued at over USD 1 billion in an all-cash transaction.

Download our Nordic SaaS valuation insights report

In our quarterly Nordic SaaS valuation insights report, we strive to provide an overview of the latest developments and trends related to valuations accompanied with our proprietary insights and learnings from live projects and observations from engaging with both clients, strategic buyers, and investors in our cross-border advisory practice.

The full Nordic SaaS valuation insights report can be downloaded by clicking the link below, and the report will also be published on our website on a quarterly basis.

Tero Nummenpää, Partner

Ruben Moring, Partner

Juuso Marttinen, Partner